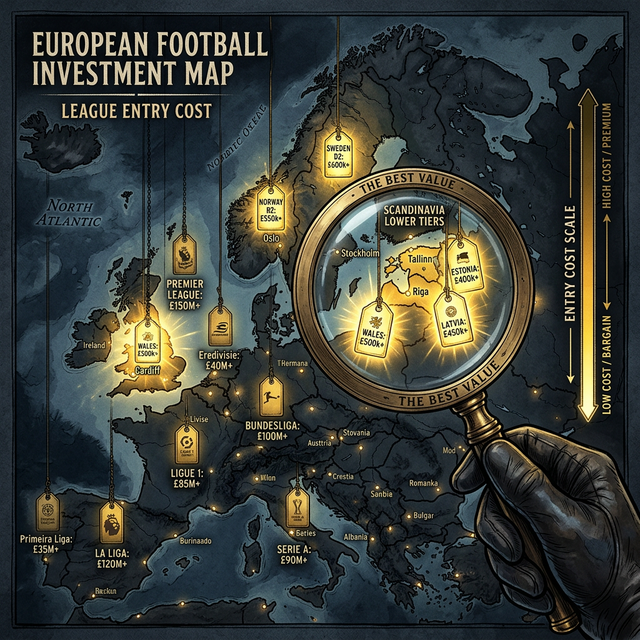

TL;DR: The Cymru Premier's average club valuation of £650K — with entry points as low as £150K — makes it one of Europe's most affordable leagues offering direct UEFA competition access. Peer leagues in Iceland, Northern Ireland, Luxembourg, and the Faroe Islands offer comparable pricing but lack Wales's combination of S4C/Sgorio broadcast infrastructure, English-language media accessibility, and the 30-50% visibility uplift from the Wrexham effect. For budget-conscious investors seeking European football assets, the data points to Wales.

The Search for Value in European Football

Football club ownership has become a global asset class. From sovereign wealth funds acquiring Premier League clubs to tech entrepreneurs buying into Serie A, the top end of the market is well-documented and increasingly expensive. But for investors seeking genuine value — clubs available for six-figure sums with direct pathways to UEFA competition — the conversation shifts to Europe's smaller football nations.

This analysis benchmarks the Cymru Premier against peer small-nation leagues across seven dimensions that matter to investors: acquisition cost, operating costs, revenue infrastructure, UEFA pathway access, broadcast coverage, growth trajectory, and regulatory environment. The conclusion is clear: the Cymru Premier offers the strongest overall value proposition, though each comparator league has specific advantages worth understanding.

For a deep dive into the Welsh market specifically, see the Club Investment Profiles, Club Valuations, and the Due Diligence Guide.

League-by-League Comparison

Headline Metrics

| League | Country | Clubs | Avg. Club Valuation | UEFA Slots | Broadcast Deal | Avg. Attendance |

|---|---|---|---|---|---|---|

| Cymru Premier | Wales | 12→16 | £650K | 4 | S4C/Sgorio (£80-120K/club) | 400-600 |

| Besta deild karla | Iceland | 12 | £500-700K | 3 | RUV (£40-80K/club) | 800-1,500 |

| NIFL Premiership | N. Ireland | 12 | £400-800K | 3 | BBC NI (£50-90K/club) | 500-1,500 |

| BGL Ligue | Luxembourg | 14 | £300-600K | 4 | Limited (£20-40K/club) | 300-800 |

| Betri deildin | Faroe Islands | 10 | £150-400K | 2 | Minimal | 200-600 |

| Virsliga | Latvia | 8 | £200-500K | 3 | Limited (£15-30K/club) | 300-800 |

| A Lyga | Lithuania | 8 | £200-400K | 3 | Limited (£10-25K/club) | 500-1,200 |

| Meistriliiga | Estonia | 10 | £150-350K | 3 | ERR (£20-40K/club) | 300-700 |

Cost of Entry

The Cymru Premier's entry-level clubs can be acquired for as little as £150K, with the average across the division at £650K. This positions it at a similar price point to Iceland and Northern Ireland, but with meaningful advantages in broadcast revenue and growth trajectory.

| Entry Point | Cymru Premier | Iceland | N. Ireland | Luxembourg |

|---|---|---|---|---|

| Lowest club valuation | ~£150K | ~£200K | ~£150K | ~£100K |

| Average club valuation | £650K | £600K | £600K | £450K |

| Highest club valuation | £3M+ (TNS) | £1.5M | £2M | £1M |

| Average transfer fee | £0-50K | £0-30K | £0-30K | £0-20K |

| Typical annual wage bill | £100-400K | £80-300K | £80-350K | £50-200K |

For club-by-club Cymru Premier valuations, see the Club Valuations report. For individual profiles, explore Bala Town (lowest cost), Caernarfon Town (best attendance), or Barry Town United (strongest brand).

What Makes the Cymru Premier Cost-Effective

1. Broadcast Revenue Floor

The S4C/Sgorio broadcast deal distributes £80-120K per club annually — the highest guaranteed broadcast income among comparable small-nation leagues. This distribution provides a revenue floor from day one, meaning even a poorly-run club has a baseline income that covers a meaningful portion of operating costs.

| League | Broadcast Revenue/Club | Coverage Quality | Language |

|---|---|---|---|

| Cymru Premier | £80-120K | Professional (TV) | Welsh/English |

| NIFL Premiership | £50-90K | Professional (TV) | English |

| Besta deild (Iceland) | £40-80K | Professional (TV) | Icelandic |

| BGL Ligue (Luxembourg) | £20-40K | Limited | Multi-lingual |

| Others | £10-30K | Minimal/streaming | Various |

For details on the Cymru Premier's broadcast landscape, see the S4C/Sgorio Broadcast analysis.

2. UEFA Competition Access

The Cymru Premier allocates four European competition slots — a generous ratio relative to league size. Champions (Conference League/Champions League pathway), cup winners, and league runners-up all qualify, meaning that clubs outside the title race still have a realistic European route.

| Competition Slot | Revenue Potential | Probability (mid-table club) |

|---|---|---|

| Champions League qualifying | £100-500K+ | Low (title required) |

| Conference League qualifying | £50-200K | Medium (top 3-4) |

| Welsh Cup winner pathway | £50-150K | Medium (knockout format) |

European qualification revenue is episodic but transformational at Cymru Premier scale. A single Conference League qualifying campaign can generate income equivalent to 15-40% of a club's annual revenue. See the European Qualification analysis for the financial breakdown.

3. The Wrexham Effect

No other small-nation league benefits from an equivalent visibility catalyst. The Wrexham AFC story — American ownership, Netflix documentary, rapid on-pitch success — has generated a 30-50% increase in global interest in Welsh football. This manifests as:

- Increased media coverage of Welsh football generally

- International investor enquiries rising year-on-year

- Sponsorship interest from brands seeking Welsh football association

- Tourism-linked matchday attendance at clubs in scenic locations

- Player recruitment advantages as Welsh football's profile rises

The Wrexham effect is not permanent, but it has created a window of elevated interest that benefits first-movers disproportionately. See the Wrexham Effect analysis for the data.

4. League Expansion

The Cymru Premier's expansion from 12 to 16 clubs in 2026/27 is a structural positive:

- More fixtures means more matchday and broadcast revenue per club

- Enhanced commercial attractiveness of a larger, more competitive league

- Increased European slots (likely) as the league gains UEFA coefficient points

- Greater squad depth requirements creating more transfer market activity

See the Expansion Guide for the full implications.

5. English-Language Accessibility

Wales operates within the UK legal and commercial framework, with English as a co-official language. For international investors — particularly from the United States, which represents the largest pool of football club buyers — this eliminates the language, legal, and cultural barriers that exist when investing in Iceland, Luxembourg, or the Baltic states. Companies House filings, FAW correspondence, and legal documentation are all in English.

For US-specific guidance, see the American Investors guide.

Peer League Deep Dives

Iceland (Besta deild karla)

Strengths: Higher average attendance (800-1,500), strong national team brand post-Euro 2016, excellent youth development infrastructure, stable economy.

Weaknesses: Geographic isolation increases travel costs for European matches, small domestic sponsorship market, Icelandic-language barrier for international investors, harsh winter climate limits the season to May-October.

Verdict: Competitive with the Cymru Premier on price and quality, but the seasonal limitations and geographic remoteness reduce commercial upside. Best suited to Scandinavian investors with existing Icelandic connections.

Northern Ireland (NIFL Premiership)

Strengths: English-language environment, BBC NI broadcast coverage, strong supporter cultures at clubs like Linfield and Glentoran, proximity to Great Britain.

Weaknesses: Sectarian dynamics create community complexity, limited growth trajectory (attendance has been flat for a decade), smaller broadcast deal than Cymru Premier, political uncertainty.

Verdict: Comparable to the Cymru Premier on cost and accessibility, but lacks the growth narrative. The established supporter bases are a strength, but the market feels mature rather than expanding.

Luxembourg (BGL Ligue)

Strengths: Wealthy domestic economy, multilingual environment, low operating costs, strong UEFA coefficient relative to league quality (punching above weight in European competition).

Weaknesses: Very low attendance (300-800), minimal broadcast infrastructure, limited sponsorship market, perception as a financial rather than sporting destination.

Verdict: The lowest-cost entry point in Western Europe, but the absence of meaningful broadcast revenue and supporter engagement makes it a pure UEFA-pathway play. Suitable for investors focused exclusively on European competition revenue.

Baltic States (Latvia, Lithuania, Estonia)

Strengths: Very low acquisition and operating costs, EU membership, growing economies, young, technically skilled player pools.

Weaknesses: Language barriers, smaller broadcast markets, limited international visibility, geographic distance from major football markets, variable governance standards.

Verdict: The cheapest options available, but with proportionally lower revenue potential and higher operational complexity for non-local investors.

The Investment Decision Framework

For investors comparing small-nation European leagues, the decision framework should weight the following factors:

| Factor | Weight | Cymru Premier Score | Best Alternative |

|---|---|---|---|

| Acquisition cost | 20% | 8/10 | Luxembourg, Estonia |

| Broadcast revenue | 15% | 9/10 | N. Ireland |

| UEFA pathway quality | 15% | 9/10 | Luxembourg |

| Growth trajectory | 15% | 9/10 | None comparable |

| Investor accessibility | 10% | 10/10 | N. Ireland |

| Operating cost efficiency | 10% | 7/10 | Baltic states |

| Supporter culture | 10% | 7/10 | Iceland, N. Ireland |

| Regulatory environment | 5% | 9/10 | N. Ireland |

| Weighted Score | 100% | 8.6/10 |

The Cymru Premier scores highest on broadcast revenue, UEFA pathway, growth trajectory, and investor accessibility. It is not the absolute cheapest option (Luxembourg and the Baltic states offer lower entry points), but the total value proposition — cost plus revenue plus growth — is strongest.

Return Projections by League

| League | 5-Year Revenue Growth (est.) | European Revenue Potential | Total Return Potential |

|---|---|---|---|

| Cymru Premier | 30-60% | £50-500K per campaign | Highest |

| Iceland | 10-20% | £50-300K per campaign | Moderate |

| N. Ireland | 5-15% | £50-300K per campaign | Moderate |

| Luxembourg | 15-30% | £100-500K per campaign | Moderate-High |

| Baltic states | 20-40% | £30-200K per campaign | Moderate |

For detailed Cymru Premier return projections, see the Investment Returns analysis. For how Welsh returns compare globally, see the Global Benchmarking report and the Small Nation Returns comparison.

Practical Considerations for International Investors

Legal and Regulatory

| Consideration | Wales | Iceland | N. Ireland | Luxembourg |

|---|---|---|---|---|

| Company registration | UK (Companies House) | Icelandic | UK | Luxembourg |

| Language of filings | English | Icelandic | English | Multi-lingual |

| FA approval required | Yes (FAW) | Yes (KSI) | Yes (IFA) | Yes (FLF) |

| Fit and proper person test | Yes | Yes | Yes | Yes |

| Visa requirements (non-EU) | UK visa rules | EEA rules | UK visa rules | EU rules |

Football-Specific

| Consideration | Wales | Iceland | N. Ireland | Luxembourg |

|---|---|---|---|---|

| Season | Aug-May | May-Oct | Aug-May | Aug-May |

| Artificial pitches | Permitted | Common | Permitted | Permitted |

| Salary cap | No | No | No | No |

| Foreign player limits | Relaxed | EU+ rules | Relaxed | EU rules |

| Academy requirements | FAW licensing | KSI rules | IFA rules | FLF rules |

Who Should Invest Where

The Cymru Premier is best for: Investors seeking the strongest overall package — broadcast revenue, growth trajectory, UEFA access, and English-language accessibility. Particularly suited to American, British, and international investors who want a hands-on ownership experience with meaningful upside.

Iceland is best for: Scandinavian investors or those with Icelandic connections who value strong supporter culture and are comfortable with seasonal limitations.

Northern Ireland is best for: UK-based investors seeking familiar regulatory and cultural environments with established supporter bases.

Luxembourg is best for: Investors focused primarily on UEFA competition access and willing to accept minimal domestic revenue.

Baltic states are best for: Investors seeking the absolute lowest entry cost and comfortable navigating non-English regulatory environments.

Conclusion

The Cymru Premier stands out among Europe's affordable football leagues because it combines low acquisition costs with meaningful revenue infrastructure, genuine growth momentum, and practical accessibility for international investors. The league's expansion to 16 clubs, the Wrexham-driven visibility surge, and the S4C/Sgorio broadcast deal create structural tailwinds that no peer league currently matches.

For investors ready to explore specific Welsh clubs, start with the Club Investment Profiles, review the Due Diligence Guide, and consult the Sponsorship Guide for commercial context. For US-based investors, the American Investors Guide addresses jurisdiction-specific considerations.

Source & Methodology

League comparisons are based on publicly available data from UEFA, national football association reports, Transfermarkt valuations, and Cymru Connect's proprietary research. Broadcast revenue figures are estimated from published deals and industry sources. Club valuations reflect Cymru Connect's modelling for the Cymru Premier and equivalent analyses for comparator leagues. Attendance data is sourced from league-published statistics and independent verification. Currency conversions use March 2026 exchange rates. All figures should be treated as informed estimates; investors should conduct independent due diligence on any specific league or club.