TL;DR: The League of Ireland generates 3-5x more revenue per club with attendances of 2,300-3,500, but acquisition costs are proportionally higher and competition for investment is fiercer. The Cymru Premier's lower entry price, consistent UEFA participation through TNS, and structural growth catalysts (16-team expansion, Wrexham effect) offer a different risk-return profile: lower absolute revenue today, but significantly greater upside potential per pound invested.

Two Celtic Leagues, Two Investment Profiles

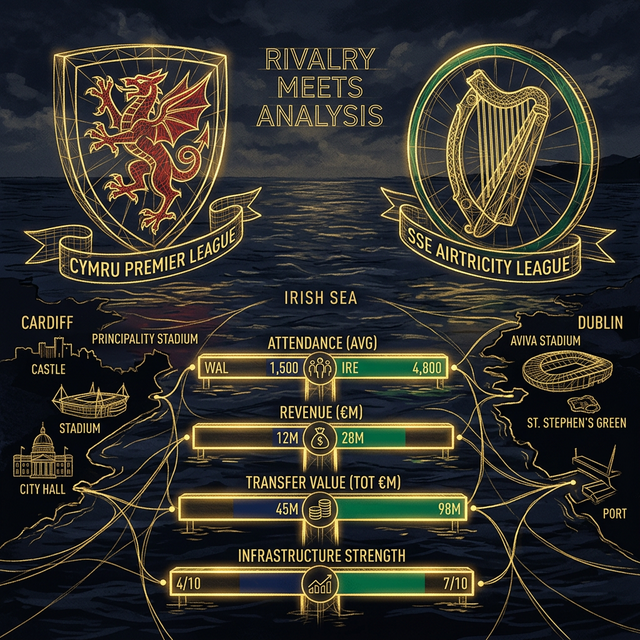

The Cymru Premier and the League of Ireland Premier Division are the two most directly comparable professional football leagues in the British Isles. Both serve small nations with passionate football cultures, both operate in the shadow of English football's commercial dominance, and both offer European competition access through UEFA coefficients that are modest but meaningful.

Yet the financial profiles diverge sharply. The League of Ireland has experienced a sustained commercial renaissance — driven by FAI investment, improved broadcast deals, and a wave of private ownership — that has pulled it ahead of the Cymru Premier on virtually every revenue metric. The question for investors is not whether Ireland is bigger (it clearly is), but whether the Cymru Premier's lower starting point and stronger structural growth catalysts make it the better value proposition on a risk-adjusted basis.

For broader cross-league context, see our Global Benchmarking report and the Cheapest Football Leagues to Invest in Europe analysis.

Financial Comparison: The Core Metrics

| Metric | Cymru Premier | League of Ireland (Premier) | Ratio (Ireland:Wales) |

|---|---|---|---|

| Number of Clubs | 12 (expanding to 16) | 10 | 0.8x |

| Average Club Revenue | £800K-1.5M | €1.5-3M (£1.3-2.6M) | 1.7-2.0x |

| Top Club Revenue | £3.2M (TNS) | €4-5M (Shamrock Rovers) | 1.3-1.6x |

| Average Attendance | 400-600 | 2,300-3,500 | 4-6x |

| Broadcast Revenue per Club | £80-120K | €150-300K (£130-260K) | 1.6-2.2x |

| Average Squad Value | ~£700K | ~€2.5M (£2.1M) | 3.0x |

| Top Squad Value | £2.5M (TNS) | €5-7M (Shamrock Rovers) | 2-2.8x |

| Estimated Acquisition Cost (Mid-Table) | £200-500K | €1-3M (£850K-2.6M) | 4-5x |

The 4-5x gap in acquisition costs is the most striking figure for investors. Buying a competitive mid-table Cymru Premier club costs approximately one-fifth of what an equivalent position in the League of Ireland would require — yet the Welsh club comes with European qualification prospects, an established domestic broadcast deal, and access to a growing market.

Attendance: Ireland's Structural Advantage

The attendance gap is the primary driver of Ireland's revenue advantage. At 2,300-3,500 average, League of Ireland clubs generate roughly 4-6x the gate receipts of typical Cymru Premier fixtures.

| Attendance Metric | Cymru Premier | League of Ireland |

|---|---|---|

| Average Attendance | 400-600 | 2,300-3,500 |

| Top Club Attendance | 820 (Caernarfon) | 5,000+ (Shamrock Rovers) |

| Stadium Capacity Utilisation | 15-25% | 40-60% |

| Year-on-Year Growth | 10-15% | 5-8% |

| Wrexham/Visibility Effect | +30-50% | N/A |

However, two factors complicate the narrative. First, Cymru Premier attendance is growing faster in percentage terms, driven by the Wrexham effect and increased media coverage. Second, stadium utilisation in Wales (15-25%) leaves far more headroom for growth than Ireland's 40-60%. A club that doubles its attendance from 500 to 1,000 generates a proportionally larger revenue increase than one growing from 3,000 to 3,500.

Our Attendance Trends analysis tracks these growth dynamics in detail.

Broadcast Revenue: Different Models, Different Trajectories

Both leagues benefit from domestic broadcast partnerships, but the structures differ significantly.

Cymru Premier: S4C/Sgorio

The Cymru Premier's deal with S4C/Sgorio delivers £80-120K per club annually. S4C's public service mandate to broadcast Welsh-language sport creates a structural floor under broadcast revenue — the deal is unlikely to disappear even in adverse market conditions. However, the limited commercial market for Welsh-language broadcasting constrains the upside.

The expansion to 16 teams increases the total number of fixtures available for broadcast selection by 82%, which should strengthen the league's negotiating position in the next rights cycle. Our S4C/Sgorio Broadcast Sponsorship report analyses the current deal structure.

League of Ireland: LOITV and RTE

The League of Ireland's broadcast ecosystem includes free-to-air coverage on RTE, the LOITV streaming platform, and international distribution deals. The combined value per club is approximately €150-300K — roughly double the Cymru Premier figure but still modest by European standards.

Ireland's larger English-speaking market gives it a structural broadcast advantage that Wales cannot fully replicate. However, the LOITV direct-to-consumer model offers a template that Cymru Premier clubs could adapt — a Welsh-language streaming platform for matches not selected by S4C could unlock additional revenue.

European Competition: Wales's Structural Edge

European competition is the area where the Cymru Premier holds a genuine structural advantage over the League of Ireland.

| European Metric | Cymru Premier | League of Ireland |

|---|---|---|

| UEFA Coefficient Ranking | ~35th | ~28th |

| Champions League Qualifying Spots | 1 | 1 |

| Conference League Spots | 1-2 | 2-3 |

| Most Successful Club | TNS (15+ seasons) | Shamrock Rovers |

| European Prize Money (Top Club) | £50-200K per campaign | €100-400K per campaign |

| Historical European Progression | 1-2 rounds typical | 1-3 rounds typical |

While Ireland's coefficient is higher and its clubs generally progress further in European competition, the Cymru Premier's consistent participation — led by TNS's remarkable run of Champions League qualifying appearances — demonstrates that European revenue is a reliable annual income stream rather than a one-off bonus.

For a detailed analysis of how European qualification drives club valuations, see our European Qualification report.

Commercial Revenue: The Sponsorship Gap

Commercial revenue is where the League of Ireland's advantage is most pronounced. Higher attendances, better broadcast viewership, and a larger domestic market combine to produce sponsorship packages that are 2-3x more valuable than their Cymru Premier equivalents.

| Sponsorship Category | Cymru Premier Range | League of Ireland Range |

|---|---|---|

| Shirt Sponsorship (Top Club) | £200-500K+ | €300-750K+ |

| Shirt Sponsorship (Mid-Table) | £40-80K | €80-200K |

| Stadium Naming Rights | £20-100K | €50-200K |

| Training Kit Sponsor | £15-60K | €30-120K |

| Total Commercial Revenue (Average) | £100-300K | €250-600K |

However, the Cymru Premier's commercial market is less competitive and more fragmented, meaning sponsors receive greater prominence and category exclusivity. A shirt sponsor of a Cymru Premier club receives genuine brand association that stands out — unlike in larger leagues where dozens of commercial partners compete for attention.

Our Shirt Sponsorship analysis provides detailed pricing and exposure metrics, while the Sponsorship Costs 2026 report covers the full commercial landscape.

Ownership and Governance

Both leagues feature a mix of private and community ownership, but the regulatory frameworks differ.

| Governance Metric | Cymru Premier | League of Ireland |

|---|---|---|

| FAW/FAI Licensing Required | Yes | Yes |

| Community Ownership | Growing trend | Established |

| Foreign Ownership | Permitted and growing | Permitted and growing |

| Financial Fair Play | Light touch | Moderate |

| Companies House/CRO Filings | Required | Required |

The Cymru Premier's lighter regulatory framework makes it easier for new investors to enter, but also provides less protection against financial mismanagement. The Due Diligence Guide covers the governance considerations for prospective acquirers, while the Companies House Filings analysis examines the financial transparency of current Welsh clubs.

Growth Catalysts: Where Wales Has the Edge

While the League of Ireland is larger today, the Cymru Premier has several structural growth catalysts that could narrow the gap over the next 3-5 years.

1. The 16-Team Expansion

The expansion from 12 to 16 teams in 2026/27 increases total fixtures by 82%, creating more broadcast inventory, more matchday events, and more sponsorship opportunities. The League of Ireland has no comparable structural change on the horizon. See our Expansion 2027 Investment analysis.

2. The Wrexham Effect

Wrexham's Hollywood-driven rise has brought unprecedented international attention to Welsh football. While the effect is concentrated on Wrexham itself, the spillover to the Cymru Premier is measurable — attendance growth of 30-50% at clubs that have capitalised on the increased visibility.

3. Digital Growth Potential

Our Digital Presence Rankings reveal that most Cymru Premier clubs have minimal digital footprints, with only 2 of 20 clubs on YouTube and none on TikTok. This is not a weakness — it is an opportunity. A focused digital strategy can produce outsized growth from a low base, driving sponsorship value and fan engagement in ways that are no longer available to better-established leagues.

4. Women's and Futsal Integration

The Cymru Premier ecosystem increasingly includes women's football (Adran leagues, 23 clubs) and futsal (7 Welsh + 19 UK clubs). These adjacent markets create cross-selling opportunities for sponsors and community engagement platforms that the League of Ireland has been slower to develop. Our Women's Football Investment Guide covers this dimension.

The Investment Decision Framework

| Factor | Favour Cymru Premier | Favour League of Ireland |

|---|---|---|

| Entry Cost | Significantly lower | Higher but more established |

| Current Revenue | Lower | Higher |

| Revenue Growth Rate | Higher (from lower base) | Moderate |

| European Access | Consistent (TNS-led) | Slightly stronger coefficient |

| Attendance Growth Potential | Very high (15-25% utilisation) | Moderate (40-60% utilisation) |

| Structural Catalysts | Multiple (expansion, Wrexham, digital) | Fewer near-term |

| Market Competition | Less competitive | More investors competing |

| Risk Profile | Higher (smaller market) | Moderate |

For investors with higher risk tolerance seeking maximum growth potential per pound invested, the Cymru Premier offers a more compelling proposition. For those prioritising established revenue streams and lower volatility, the League of Ireland provides a safer but more expensive entry point.

Conclusion

The Cymru Premier and League of Ireland are not competing for the same investors — they serve different risk-return appetites. Ireland offers 3-5x the revenue at 4-5x the acquisition cost, with more established commercial platforms and higher attendances. Wales offers lower absolute returns but dramatically cheaper entry, stronger growth catalysts, and the possibility of outsized appreciation from a lower base. The most informed investors will evaluate both leagues and allocate based on their specific return requirements, timeline, and appetite for growth-stage risk.

Analysis based on FAW and FAI annual reports, Companies House and CRO filings, Transfermarkt data, UEFA coefficient tables, and Cymru Connect internal modelling. Revenue and valuation figures are estimates based on publicly available information. Currency conversions use approximate March 2026 exchange rates. Data as of March 2026.